What's in your wallet?

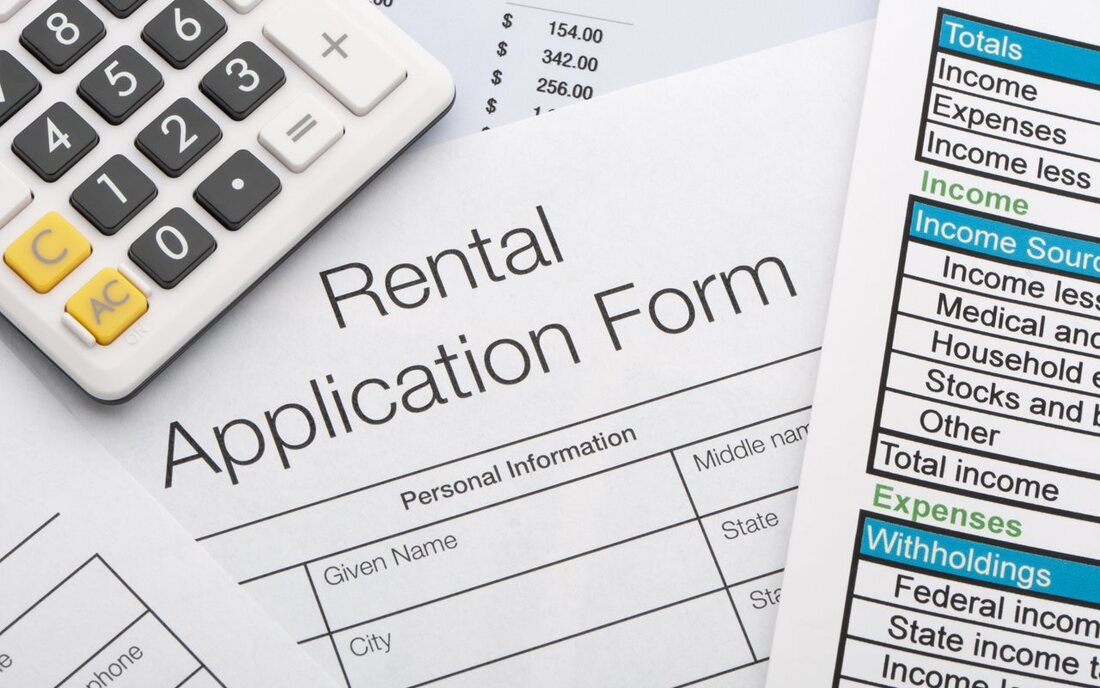

Where is application fraud on the rise? Check out the 'Treacherous 20' cities(BPT) - Evictions have been front-page news during the pandemic. At the start of the pandemic, the National Low Income Housing Coalition estimated that without assistance, 30 to 40 million Americans would be in danger of eviction by the end of that year. It’s a heart-wrenching situation, which was largely avoided through widespread eviction moratoriums around the country. But there is another side to the eviction crisis: Criminals actively trying to get into apartments they have no ability (nor intention) to pay for. Their modus operandi is to submit fake pay stubs and bank statements to convince landlords they have the means required to afford the rent. One in eight paystubs or bank statements submitted to apartment owners are fake today. Fraudsters submitted more than 10 million fake financial documents last year. It is called application fraud, and experts estimate that this crime accounts for one in four of all evictions. Snappt, a business with expertise in spotting fake financial documentation, has scanned several million pay stubs and bank statements. Based on a deep analysis of these documents, they have released their “Treacherous 20” list — the list of the top 20 major metropolitan areas by application fraud rate. The Snappt Treacherous 20 The top 20 major metropolitan areas by application fraud rate: 1) Atlanta - 17.9% Note that the eviction rates — which are often driven by application fraud — ran as high as one in nine for the Treacherous 20. The average eviction rate was 4.83%, nearly double the national average of 2.6%. In Atlanta, property managers are seeing fake paystubs or bank statements every fifth or sixth applicant. Houston and Dallas were not far behind. Drivers of application fraud There are many drivers of application fraud, but rent increases and unemployment stick out. Many of the Treacherous 20 show extreme movement along these drivers.

A post-pandemic world The pandemic was tough for everyone. While eviction moratoriums kept many renters safe, owners faced high losses. And, as application fraud soars, the risk to owners is getting even higher. Solutions like Snappt help protect landlords. Follow your credit repair progress with the all new CreditRepair app. Take advantage of a variety of tools to help understand and improve your credit, right from your mobile device. How credit repair works? We challenge your questionable negative items with all three bureaus, ensuring your credit reports are accurate and fair. We ask your creditors to verify the negative items they’re reporting. If they can’t, they are required by law to stop reporting them. We continue to watch your credit, addressing additional issues as they arise so that you can stay on track and reach your goals.

0 Comments

Cómo reabastecer su kit de emergencia para la diabetes antes de fin de año(BPT) - El fin de año se acerca a pasos agigantados. Para los pacientes que viven con diabetes, es un buen momento para revisar su kit de emergencia y reabastecerlo con cualquier suministro y receta pertinente, para aprovechar al máximo sus beneficios de seguro médico. La conclusión del año equivale a que su deducible de seguro y su cuenta flexible de gastos (FSA) se reprogramarán en breve con vistas a un nuevo período. Ahora es el momento de verificar si ha alcanzado el deducible. De ser así, haga una lista de los medicamentos y suministros que puede comprar con su FSA para satisfacer sus necesidades en casa y cuando esté de viaje. Un dispositivo cuya compra podría considerar para finales de este año es una pluma de rescate de glucagón como Gvoke HypoPen® (inyección de glucagón). Si experimenta un nivel bajo de azúcar en la sangre, puede resultarle difícil hacer la mezcla de su propio glucagón. En su lugar, opte por esta inyección premezclada y lista para usar, que todos los pacientes con tratamiento de insulina deben tener en su kit de emergencia. Si bien el proceso de controlar su diabetes puede ser estresante y costoso, ahorrar en algunos de sus gastos de atención médica puede aliviar parte de esa carga. No hay duda de que le alegrará contar con esta conveniente pluma de rescate como red de seguridad para cuando más la necesite. Hable con su médico sobre la adición de Gvoke HypoPen® a su kit de herramientas para la diabetes antes de que expiren los fondos de la FSA, y reprogramen su deducible. Para obtener más información, visite GvokeGlucagon.com. INFORMACIÓN DE SEGURIDAD IMPORTANTE SOBRE GVOKE INDICACIONES Y RESUMEN DE SEGURIDAD GVOKE es un medicamento recetado que se usa para tratar niveles muy bajos de azúcar en la sangre (hipoglucemia grave) en adultos y niños mayores de 2 años que tienen diabetes. Se desconoce si GVOKE es seguro y eficaz en niños menores de 2 años de edad. ADVERTENCIA No utilice GVOKE si:

GVOKE PUEDE CAUSAR EFECTOS SECUNDARIOS GRAVES COMO: Hipertensión. GVOKE puede causar presión arterial alta en ciertas personas con tumores en sus glándulas suprarrenales. Bajos niveles de azúcar en la sangre. GVOKE puede causar niveles bajos de azúcar en la sangre en ciertas personas con tumores en el páncreas (insulinomas) que surgen al producir demasiada insulina en el organismo. Reacción alérgica grave. Llame a su médico o busque ayuda de inmediato si tiene una reacción alérgica grave como:

EFECTOS SECUNDARIOS COMUNES Entre los efectos secundarios más comunes de GVOKE en los adultos están:

Entre los efectos secundarios más comunes de GVOKE en los niños están:

Le advertimos que estos no son todos los posibles efectos secundarios de GVOKE. Para obtener más información, consulte con su médico. Llame a su médico para obtener asesoramiento sobre los efectos secundarios. Se le recomienda que informe los efectos secundarios de los medicamentos recetados a la Administración de Alimento y Medicamento (FDA, por sus siglas en inglés). Visite el sitio web www.fda.gov/medwatch o llame al número telefónico 1-800-FDA-1088. ANTES DE USARLA Antes de usar GVOKE, comuníquele a su médico todos sus trastornos, incluyendo si:

Informe a su médico sobre todos los medicamentos que toma, incluidos los recetados y los de venta libre, las vitaminas y los suplementos confeccionados con hierbas. MODO DE EMPLEO

CÓMO ALMACENARLA

Mantenga GVOKE y todos los medicamentos fuera del alcance de los niños. Para obtener más información, llame al 1-877-937-4737 o visite www.GvokeGlucagon.com.

Adevertisement Only Below:

Start Your Own Business Funding Agency and help fuel business owners with working capital or savings. To learn more click this banner

Cómo ahorrar con Amazon Access: el nuevo centro para compras accesibles de Amazon(BPT) - Amazon puso en marcha recientemente Amazon Access, un nuevo centro para que los clientes exploren programas, descuentos y características que hacen aún más fáciles y asequibles las compras en Amazon. Debido al difícil clima económico existente, y a que muchas personas están enfrentando costos crecientes en necesidades esenciales, Amazon está introduciendo ofertas aún más accesibles en su sitio web para todos los clientes, sin importar sus circunstancias. A continuación, varias maneras en que puede comenzar a ahorrar hoy mismo con Amazon Access:

Advertisement Only Below

OmahaSteaks.com, Inc. click here to see Bigdoggpinc's offer!

Business Funding (from $1,000 - $2,000,000) or Employee Tax Credits (up To $26,000 Per Employee)

No deje que el final de 2022 sabotee sus resoluciones de Año Nuevo(BPT) - ¿Alguna vez ha pensado que, como al día siguiente comenzará un nuevo estilo de vida saludable, puede echar por tierra todos sus objetivos sanos, aunque sea por un día? Si es así, no está solo. En la medida que termina un año y se acerca uno nuevo, muchas personas que consideran resoluciones relacionadas con la salud ya están “cancelando” el final del año. Según la quinta encuesta anual Writing Off the End of the Year de Herbalife Nutrition, el 60% de los quienes proyectan posponer el inicio de sus hábitos saludables hasta el nuevo año ya han comenzado a hacerlo, admitiendo que su límite es a mediados de noviembre. Y desafortunadamente, el 25% de los estadounidenses todavía tienen el peso que ganaron a fines del año anterior, perpetuando un ciclo de autosabotaje difícil de romper. El estudio, que encuestó a 2,000 estadounidenses y a 2,750 participantes de cinco países diferentes, reveló que más de la mitad (53%) admitió haber roto sus dietas al final del año, mientras que el 37% citó como causa específica las tentaciones de comida festiva. El encuestado promedio afirmó que espera ganar cinco libras y media antes de 2023, además de cualquier peso corporal que todavía acumule de la temporada festiva pasada. Los objetivos de salud siguen siendo prioritarios Según la encuesta, las personas que piensan en las resoluciones del próximo año siguen dándoles prioridad a la salud, la nutrición y el bienestar. Estas son las principales resoluciones de Año Nuevo para 2023: 1. Ahorrar más dinero: 57% Pero lamentablemente, permitirse los excesos de la temporada festiva a fines de 2022 podría hacerle más difícil el logro de sus elevados objetivos de salud. De hecho, casi la mitad de los encuestados (49%) declararon que planeaban esperar hasta el nuevo año para tratar de perder peso. ¿Hasta dónde llegamos cuando se “cancelas” el final del año? A continuación, las principales respuestas de la encuesta con respecto a hasta qué punto sus participantes admitieron haberse dejado llevar al final del año:

Luego de ver la lista anterior, tendrá claro que “cancelar” el final del año podría sumar muchos hábitos que deberá cambiar después de concluir la fiesta de Año Nuevo. ¿Por qué no prepararse entonces para el éxito? Este año, en lugar de “cancelar” el final del año, podría cambiar el ciclo de excesos festivos con un poco de planificación inteligente y medidas con sentido común. ¿El resultado? Sus resoluciones de Año Nuevo comenzarán desde una posición de fuerza, con mucho menos peso que perder o hábitos que cambiar el 1 de enero. Estos son algunos consejos del Dr. Kent Bradley, director de salud y nutrición de Herbalife Nutrition, para ayudarlo a pasar las fiestas y evitar ese sabotaje de salud de fin de año:

Estos consejos demuestran que todavía es posible disfrutar de las fiestas de fin de año sin eliminar de plano todos sus objetivos de salud. Comience ya Si se propone comenzar 2023 con una actitud de “Año Nuevo, un nuevo yo” como el 63% de los encuestados, evite la trampa del sabotaje desde ahora siendo más consciente de sus hábitos durante las vacaciones. Su nuevo yo de 2023 se lo agradecerá. Mediante Herbalife Nutrition, una compañía con propósito, los distribuidores brindan a los clientes un conocimiento, aliento, respeto, orientación de apoyo y comunidad irremplazables. Les damos todos un camino más simple para vivir un estilo de vida saludable y activo. Obtenga más información sobre los buenos hábitos de salud en IAmHerbalifeNutrition.com.

Advertisement Only

The Employee Retention Credit (ERC) is a Payroll Tax Credit designed to reward businesses for retaining employees during COVID-19. The credit was initially signed into law March 2020 as part of the CARES Act. The credit was later expanded upon with the Consolidated Appropriations Act in December 2020 and the American Rescue Plan Act in June 2021.

Business Owners can receive a refundable credit up to $5,000 per employee in 2020, and $7,000 per employee, per quarter (excluding the 4th quarter), in 2021 for qualified wages. This can total up to $26,000 per employee. Learn more

Mission fraud-free: 11 ways veterans can ward off scammers(BPT) - While identity theft and similar scams are a problem for many Americans, U.S. veterans face a higher-than-average risk of falling victim to that kind of fraud. Statistics back that up. For example, of the 200,000 reports of fraud the FTC received from military members in 2021, 78% came from military retirees and veterans. And an AARP survey shows that a whopping one-third of vets targeted by service-related scams have lost money in those scams. What’s going on? Unfortunately, vets and their families are prime targets for fraudsters, in part because they receive special benefits and in part because while enlisted, they frequently changed residences. Past data breaches have also led to leaks of their personal information that make the problem worse. The good news is that vets can follow these 11 suggestions for protecting themselves and their families from fraud. 1. Practice skepticism. Be suspicious of unexpected calls, emails or text messages that demand action from you. Fraudsters often masquerade as legitimate organizations by creating authentic-seeming caller IDs, email addresses and websites; for example, their email addresses may be similar to those you know and trust, but they’ll be off by one letter — or they’ll end with .net instead of .com, .gov or .org. When in doubt, don’t click on the provided link or attachments or follow their directions; instead, end communications and contact the real organizations directly via the number listed on your latest bill or their official website to check whether the sketchy-seeming communications are legitimate. 2. Protect your private data. Be wary about sharing or allowing others to overhear your family’s Social Security numbers (SSNs), birth dates or other personal info. Provide the data only when necessary, then confirm how it will be secured. Black-out personal info on any forms you wish to use to access discounts. 3. Create a family code word. Provide that word to the legitimate banks, insurance providers and organizations with which you work so they can easily prove they’re not fraudulent. 4. Review account statements and credit reports. Regularly look over financial, medical and other statements. Every four months, request and read one of the free credit reports offered by Equifax, Experian and TransUnion. Follow up on any questionable charges or other discrepancies. 5. Set up free fraud alerts. Any of the three credit bureaus can arrange for you to be automatically contacted in the event of suspicious charges. 6. When in doubt, freeze your credit. If you’re experiencing identity theft or other possible fraud, a freeze will keep criminals from further accessing your credit. 7. Protect sensitive documents. Shred or keep safe papers containing personal info, including tax forms, birth certificates, Social Security cards, bank account statements and military benefit forms. 8. Be strategic about passwords. Use complex and different passwords, or even "pass-phrases" for each online account, incorporating multiple digits, upper- and lower-case letters and special characters. Stay away from obvious words like pets’ names, your hometown or your favorite sports team. Never write them down. A password manager tool can help you keep them all straight. 9. Forward your mail. Have all mail forwarded when you move or relocate so credit card offers and other documents with potentially private data don't fall into the wrong hands. 10. Set up an active-duty credit alert. For active-duty service members, ask one of the three credit bureaus to mark your file with this free, one-year alert. It encourages lenders and creditors to take extra steps to verify your identity before approving new or additional credit. Your name will also be removed from pre-screened credit card or insurance offers for two years. 11. Know the signs of identity theft. Indicators may include a lost ID; unfamiliar charges on your bank or credit card statements; credit score issues, calls trying to verify unfamiliar purchases; unfamiliar medical bills; mail theft; suspicious logins to your social media accounts; unrecognized account authentication messages; the arrival of unfamiliar bills or packages; or even warrants for your arrest. Looking for even better peace of mind when it comes to fraud protection? Aura’s user-friendly, all-in-one digital security platform continually monitors your credit, financial transactions, bank accounts, SSN, the dark web, home and title use, and criminal and court records to help keep your finances and identity safe and secure. As added protection, Aura’s U.S.-based customer service team is available for problem resolution 24/7, and each customer is backed by a $1 million identity theft insurance policy for eligible losses. Aura thanks military members, veterans and their families for their service and sacrifices by offering a two-week free trial and up to 50% off protection plans. Visit aura.com/veterans for more info.

Bigdoggpinc's Advertisement Below:

Three Financial Health Hacks To Start The School Year Strong(BPT) - With the start of a new school year underway, your teens are already learning new skills. While most of this learning happens in the classroom, there are plenty of opportunities at home to learn other life skills, especially around financial responsibility. If you haven't had money conversations with your teen, the fall semester is a great time to start. Your student will have plenty of expenses for school, extracurricular activities and their own wants and needs that they'll need to learn how to fund. These additional expenses can be a great entry point into a conversation around how to help them navigate while they cultivate their own financial skills. Not sure where to start? Check out these three financial hacks to start the school year strong. 1. Work Together It's never too late (or too early) to talk about spending mindfully and saving regularly with your children. The earlier teens learn the basics of money, the more prepared they'll be for their own financial journey. While finances can seem like an overwhelming subject for you to teach and your teen to absorb, working together and having a real-life scenario will make it easier. Teach them that conscious spending is crucial to their overall financial health. For example, they may not be aware that they're spending more on their morning latte or online shopping than they'd like. Regularly checking in with your student about their account activity keeps finances part of your family conversations. This also provides an opportunity to help them analyze how much they're earning, what they're spending it on and their savings goals. Getting started with a bank account early will help set kids on the right path for future financial success. As your child ages, Chase has different options to help on their financial journey, such as Chase High School Checking and Chase College Checking accounts. 2. Expense the Unexpected With the school year in full swing, unexpected purchases for classes beyond the standard supplies can put a dent in family finances. A study published in 2022 by the Federal Reserve found that the overall share of adults who would cover a small emergency expense using cash or its equivalent has increased to the highest level since 2013 when the survey began. This is likely because these adults were able to increase their savings to cover surprise costs. It's important to explain to your student that an emergency fund can provide peace of mind to help with life's unexpected surprises. Don't be afraid to start small, as long as you start saving; even if it's just $1 per day, you're creating a resource for emergency expenses. The easiest way to start an emergency savings fund is to automate the process. With Chase Autosave, you can set up a repeating, automatic transfer from your Chase checking into your Chase savings account. Just set the amount to be transferred, forget it and watch your savings grow. 3. Stay on Track Teaching your student how to create and stick to a budget can help them prioritize their spending and savings habits. For example, while it might be tempting to dip into an emergency fund for a new sport, band uniform or an outfit for the homecoming dance, these aren't true emergencies. Instead, students should look at their budget and plan for those significant expenses by cutting back spending in other categories for the month. The desire for these costly items also provides a great opportunity to teach your child about financial goals. If they'd like to save for a new laptop or the latest shoes, you can help them create savings goals for these expenses. This way, they can put aside a little money from each paycheck to afford the items on their wish list. Using these three tips, you can teach your child important financial skills and set them up for monetary success as they age. To learn more about high school and college checking and savings accounts, visit chase.com/studentbanking. Don't forget to check out the Chase Student Resource Center to learn more about financial health beyond spending, saving and budgeting. Bank deposit accounts, such as checking and savings, may be subject to approval. Deposit products and related services are offered by JPMorgan Chase Bank, N.A. Member FDIC

Bigdoggpinc's Advertisement Below:

|

Click me to join today!

Agent ID# 102545187Hello, I see many advertisments on many social platforms. What I can agree on my network is on fire. We are helping people more than you can realize. My business is also located in the California area. So I get the love back from my community. I am a home based business owner since Sept 19th, 1999. I just wanted to introduce myself because I am in business capital and we love to help small businesses like yours get working capital for growth, or expansion, or even to get through a tight pinch! So I just wanted to introduce myself, Leonard Bigdoggpinc Lindsey in case you are ever in the need for business working capital. When the banks can't help we usually can. :) If you ever want to talk, I'm happy to talk by phone or text +1 (310) 462-7030 by email if you prefer? [email protected] You can also learn more about my company and services. Archives

April 2024

The Rapid Finance Guide to Finding the Right Loan for Your Business Needs

Small business financing can serve many purposes, including: Startup capital Working capital to run operations Cover cash flow deficiencies Cash to cater for emergencies such as Covid-19 Money to buy another business Funding to expand your business Refinancing debt Get your funding Learn more

Incredible Healthcare options

Business Capital

Do it tired. Just do it!

When The Big Banks Can't Help, We Can!

Leaders are coming here!

Top Car Rental Picks

Do you own a business?

Categories |

RSS Feed

RSS Feed